Credit Market Collapse Has Started - The Bond Market Knows

The Fed Knows

“The comments from our Reserve Bank colleagues and CEOs they talk to are pretty constructive on the economy right now.

…This is, this, you know, this is a strong economy. We think that the economy and we think our policy are both in a very good place.

Very good place.”

Jerome Powell, Federal Reserve Chairman

November 7, 2024 FOMC Press Conference

While the Fed and other central bankers appear to be celebrating their rate policies and the debt-dependent economies they have created, there is something very different churning below the surface.

The most leveraged citizens and corporations are being intensely squeezed.

Food Banks Canada completed a survey of 4,600 people across Canada this past summer that shows 25% of respondents experienced monthly deprivation of two or more items important to maintaining a minimum standard of living (eg. paying bills, dental care, clothing, etc.).

After intense and coordinated inflationary monetary policies by central banks globally during the COVID fright, housing prices in the US and Canada remain at or near all-time highs.

Food price increases globally have shown not to be transitory and are moving higher once again:

Figure 1 - World Food Price Index; source: UN

US price inflation remains elevated above the Fed’s adjusted 2% target (core inflation rose to 3.3% in September 2024) threatening to move higher generally as central banks loosen once again:

Figure 2 - US Current CPI Inflation vs. 1970s CPI Inflation; source: blog.rangvid.com

Chairman Powell claims that goods price inflation is caused by shortages but can’t explain why, once shortages are reduced, prices do not come back down to their former levels. In reality, most know well that price inflation is an artifact of central planning of interest rates and loose monetary policy.

Under The Hood, Things Are Worse Than Promoted By Monetary Central Planners

Back in August 2022, this writer observed that the Fed (in fact, all central banks) was initiating collapse of the economy by raising interest rates after blowing, over decades, the largest monetary and debt bubble in history.

Total US debt in all sectors amounts to $99.8 trillion (T) and sustaining rates at 5% will over time impose a $5T per annum interest burden on the US economy. The math just doesn’t work.

It is therefore concerning that since the Fed’s announcement on September 18, 2024 that rates would be reduced by 0.50%, that, instead, US Treasuries in 2 Year and longer maturities have sold off driving their interest rates higher - not lower.

Figure 3 - US 2, 10 and 30 Year Treasury Yields; source: tradingview.com

The concern mentioned here and by other observers is that the Fed could be losing control of bond market yields. This potentially will force the Fed back to Quantitative Easing whereby the Fed prints currency and buys bonds to fake their prices and drive bond yields lower. Of real concern is that already elevated goods price inflation will then spike higher as in the 1970s.

Looking under the hood in the debt markets, it is clear that the consequences of higher interest rates at the current record debt burden created by central bank low rate policies, enabled by capping gold and silver prices starting in 1987, are already showing in some credit sectors.

Rising bond yields in private debt markets reflects both rising inflation risk as well as rising default risk and we would expect the most vulnerable consumer and corporate borrowers to be the first to signal incipient failure from higher rates - and that is what we are seeing.

Looking to the condition of Middle America generally away from the coastal money centers as exemplified by small bank credit card delinquency rates, we can see that small town America is already suffering with higher interest rates with card delinquency now approaching 8% - the highest since this data point was first tracked in the early 1990s:

Figure 4 - Delinquency Rate on Credit Card Loans, Banks Not Among the 100 Largest in Size by Assets; source: St. Louis Fed

The rising personal delinquency rate on credit cards is no surprise as personal interest payments have shot up by $200 billion (B) per annum since early 2020.

Figure 5 - Personal Interest Payments; source: St. Louis Fed

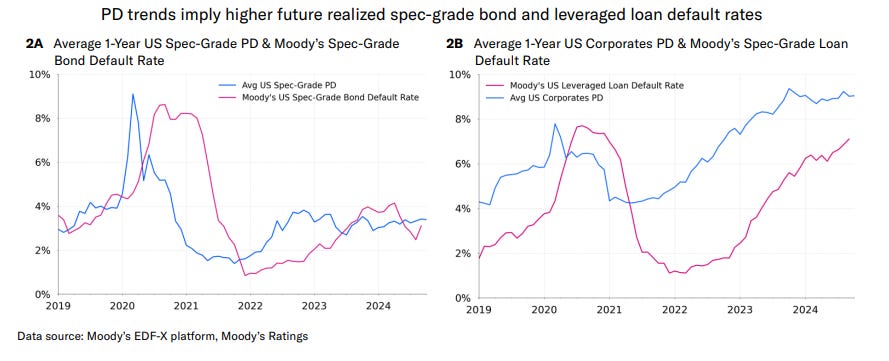

On the corporate side, the highest risk borrowers are leveraged loan borrowers where a leveraged loan is one that lenders extend to companies or individuals that already have considerable amounts of debt or a poor credit history.

The probability of default (PD) for leveraged loans can be seen to be trending higher in graph 2B below.

Note below that forward-looking PDs for Average US Corporate Borrowers (blue lines) and the Moody’s realized trailing 12-month default rates (magenta lines) for Leveraged Loan borrowers in graph 2B tell us that we are likely to see materially higher default rates than we are currently experiencing - for both - and likely default migration to other credit sectors.

The result will then be HIGHER RATES and then likely materially looser central bank monetary policy with QE.

We can thus begin to see why interest rates have started to rise even as the Fed cuts overnight rates and that this is a worrying signal. Default. Inflation.

Figure 6 - Probability of Default Trends (2B) for Leveraged Loans (magenta - 12 month trailing) and Average US Corporates (light blue - forward looking) source: Moody’s

Central Planning of Interest Rates Doesn’t Work

Central planning of interest rates was never going to work, especially if the inflationary warning signals of gold and silver prices are intentionally muted, as they have been.

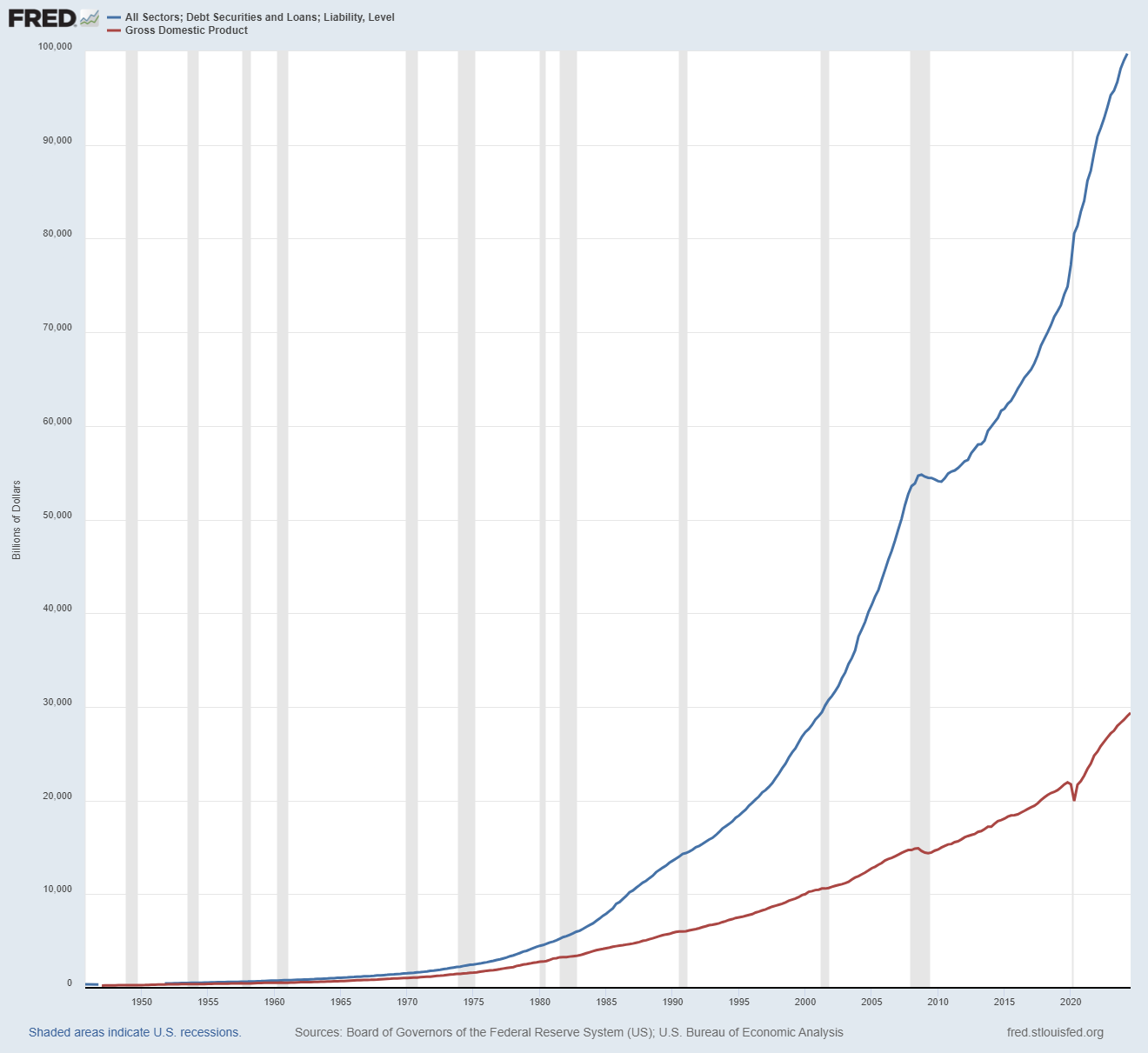

By inspection it can be seen that the idea of being able to create real growth with loose monetary policy is fictitious as the rate of growth of debt with loose monetary policy is now growing nearly asymptotically with comparatively subdued GDP growth:

Figure 7 - All Sector US Debt (blue line) [billions] vs GDP (red line) [billions p.a.]; source: St. Louis Fed

In Closing

Austrian School economists have warned for more than a century that real growth cannot be created by expanding our debt-based currency as it leads to consumption growth beyond productive output growth of the economy and, if a debt-based consumption increase is continued, such monetary expansion leads to collapse.

Central planning of currency, where central banks allow currency and debt expansion to drive expansionary government policy and central banks also served to act as financial bubble inflators and then provided gambling insurance to bail-out the financial sectors when these bubbles collapsed, is over. The Greenspan Put party is over.

Think silver. Think gold.

Best regards,

David Jensen

"Think silver. Think gold." I like your way of thinking, David. Some say Greenspan thought the same way long ago, but that he had no choice when asked and tasked with delaying the inevitable for as long as possible. Perhaps, he covertly tried hastening the utter destruction of the current monetary and financial system through his bubble-blowing methods, in order to leave no choice but to rely once again on gold and silver in the aftermath.

Although, I wonder if Greenspan thought his "Put Party" would be continued this far and long after he left?

Nonetheless, The Fed bartenders since Greenspan have been watering down their product ever more and the party goers being served are sobering up and realizing it. Now they wanna pay less, but the debt drunkards desperate to stay and too dumb to leave will have to down more of it even faster.

Ive got nearly 50% of my savings, SIPP and investments in gold and silver.

I agree with your reasoning and thank you for imparting your extensive knowledge and experience to us novices to try to help us preserve our wealth!